Car insurance can feel like a yearly burden. You pay thousands and hope you never use it.

But here’s the truth—most people overpay without even knowing it.

The good news? There are simple, smart ways to get cheap car insurance without losing protection.

Let’s uncover those secrets.

Why Car Insurance Prices Vary So Much

Two people with the same car can pay very different premiums.

Why?

Because insurers look at:

- Your driving history

- Car model and age

- City you live in

- Coverage type

- Claim history

Once you understand this, you can start controlling your premium.

Secret #1: Master the No Claim Bonus (NCB)

This is the easiest way to save money.

How NCB Works:

- No claims = discount on renewal

- Starts at 20%

- Goes up to 50%

Smart Trick:

Avoid small claims. Protect your NCB and enjoy bigger discounts later.

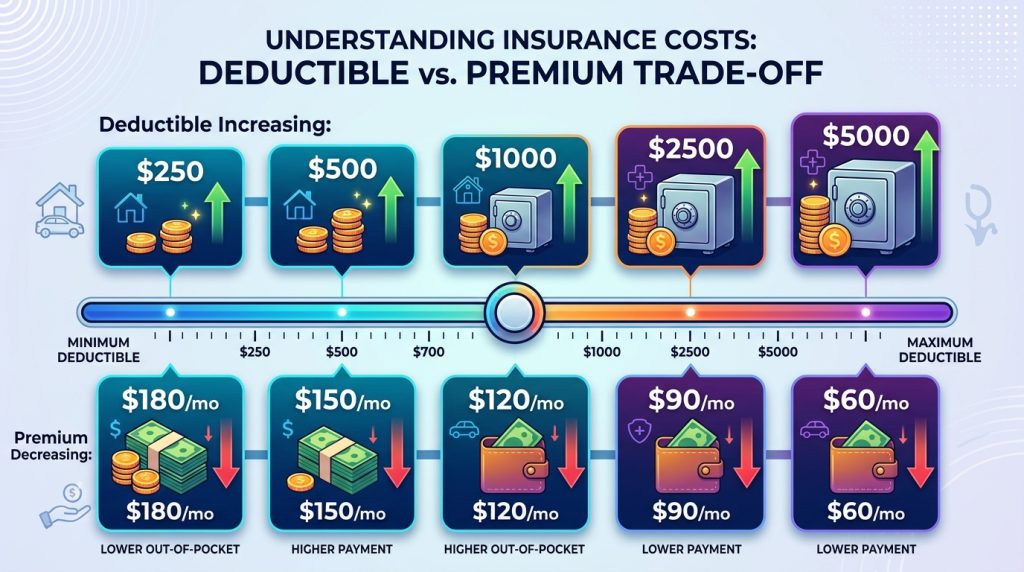

Secret #2: Increase Your Deductible Wisely

A deductible is what you pay during a claim.

Why It Helps:

- Higher deductible = lower premium

But Don’t Go Too High:

Choose an amount you can afford easily.

Balance is the key.

Secret #3: Choose the Right IDV (Don’t Overpay)

IDV = Insured Declared Value (your car’s current value).

Common Mistake:

Keeping IDV too high.

What Happens:

- Higher IDV = higher premium

Smart Move:

Set a realistic IDV based on your car’s market value.

Secret #4: Buy Insurance Online

Offline agents often include commissions.

Online Benefits:

- Lower prices

- Easy comparison

- Instant policy

You can save 10–20% instantly just by going online.

Secret #5: Pick Only Useful Add-Ons

Add-ons sound great, but they cost extra.

Popular Add-Ons:

- Zero depreciation

- Engine protection

- Roadside assistance

Smart Rule:

Only keep what you need.

Example: Old car? Skip zero depreciation.

Secret #6: Install Anti-Theft Devices

A safer car means lower risk.

Devices That Help:

- Car alarm

- GPS tracker

- Steering lock

Insurers reward this with discounts.

Secret #7: Compare Every Year (Don’t Be Lazy)

Loyalty doesn’t always pay.

What Most People Do:

Auto-renew same policy.

What You Should Do:

- Compare at least 3 insurers

- Check features + price

Switching can save thousands.

Secret #8: Maintain a Clean Driving Record

Your behavior matters.

If You:

- Avoid accidents

- Follow traffic rules

You become a low-risk driver.

Result? Lower premium over time.

Secret #9: Bundle Policies for Discounts

Buy multiple policies from one insurer.

Example:

- Car + bike

- Car + health insurance

You may get special discounts.

Secret #10: Renew on Time (Never Miss It)

Late renewal can cost you:

- Loss of NCB

- Higher premium

- Inspection fees

Easy Fix:

Set a reminder before expiry.

Quick Savings Table

| Strategy | Potential Savings |

|---|---|

| No Claim Bonus | Up to 50% |

| Online purchase | 10–20% |

| Higher deductible | 5–15% |

| Removing add-ons | ₹1,000–₹5,000 |

| Comparing plans | ₹2,000–₹7,000 |

Real-Life Example

Let’s say your premium is ₹18,000/year.

By doing this:

- Keep NCB → Save ₹6,000

- Buy online → Save ₹2,000

- Adjust IDV → Save ₹2,000

👉 Total savings = ₹10,000 per year

That’s almost 50%!

Common Mistakes That Increase Premium

Avoid these traps:

- Claiming for small damages

- Choosing too many add-ons

- Not comparing plans

- Over-insuring your car

- Missing renewal date

Pro Tips Most People Don’t Know

- Choose long-term policies for better rates

- Check festive or seasonal discounts

- Use voluntary deductible smartly

- Read policy terms before buying

FAQs (People Also Ask)

1. What is the cheapest way to get car insurance?

Maintain NCB, compare plans online, and avoid unnecessary add-ons.

2. Does NCB really reduce premium?

Yes, it can reduce your premium by up to 50% over time.

3. Is online car insurance cheaper?

Usually yes, because it cuts agent commissions.

4. Can I change insurer and keep NCB?

Yes, your No Claim Bonus can be transferred.

5. What is the biggest mistake people make?

Not comparing policies and overpaying for the same coverage.