Freelancing gives you freedom. No boss. No fixed hours. Work from anywhere.

But here’s the truth—you’re on your own.

No company benefits. No safety net. One problem, and your income can stop overnight.

That’s why insurance for freelancers is not optional anymore—it’s survival.

The Hidden Risks Freelancers Face

When you work a job, your company handles a lot:

- Health insurance

- Accident coverage

- Income protection

As a freelancer, you get none of that.

Real Risks Include:

- Sudden illness

- Client disputes

- Payment delays

- Equipment damage

- Income loss

One unexpected event can shake your entire financial life.

What Insurance Does for Freelancers

Think of insurance as your backup plan.

It helps you:

- Protect your income

- Cover medical costs

- Handle legal issues

- Keep your business running

Without it, you’re taking a big risk every day.

1. Health Insurance: Your First Priority

Medical costs are rising fast. Even a small treatment can cost thousands.

Why It Matters:

- Freelancers don’t have employer coverage

- Hospital bills can destroy savings

What to Look For:

- Cashless hospitals

- Pre & post hospitalization cover

- At least ₹10–20 lakh coverage

2. Income Protection Insurance

What if you can’t work for 2–3 months?

No work = no income.

This Insurance Helps:

- Provides monthly payout

- Covers loss of earnings due to illness or injury

It’s like getting a salary even when you’re not working.

3. Professional Liability Insurance

Also called Errors & Omissions (E&O) insurance.

If a client claims:

- Your work caused loss

- You made a mistake

You could face legal trouble.

This Insurance Covers:

- Legal costs

- Compensation claims

Especially important for:

- Designers

- Developers

- Consultants

- Marketers

4. Equipment Insurance

Your laptop, camera, or tools are your lifeline.

Risks:

- Theft

- Damage

- Accidents

Coverage:

- Repair or replacement cost

Perfect for:

- Photographers

- Video editors

- Content creators

5. Life Insurance (For Financial Security)

If you have dependents, this is a must.

Why You Need It:

- Protects your family financially

- Covers loans and liabilities

Best Option:

- Term insurance (low cost, high coverage)

6. Personal Accident Insurance

Accidents can happen anytime.

Covers:

- Disability

- Injury

- Death benefits

Even a minor accident can stop your work.

Types of Insurance Freelancers Should Consider

| Insurance Type | Why It’s Important |

|---|---|

| Health Insurance | Covers medical expenses |

| Income Protection | Replaces lost income |

| Liability Insurance | Handles legal claims |

| Equipment Insurance | Protects tools |

| Life Insurance | Secures family |

| Accident Insurance | Covers injuries |

How Much Insurance Do Freelancers Need?

It depends on your lifestyle and income.

Basic Rule:

- Health Insurance: ₹10–20 lakh

- Life Insurance: 10–15x annual income

- Emergency fund: 6 months expenses

Common Mistakes Freelancers Make

Avoid these:

- Thinking “I’m healthy, I don’t need insurance”

- Relying only on savings

- Ignoring legal risks

- Choosing cheapest plans

- Not reading policy details

Smart Tips Before Buying Insurance

- Compare plans online

- Read reviews and claim ratios

- Start early (lower premium)

- Choose only relevant coverage

- Update policies as income grows

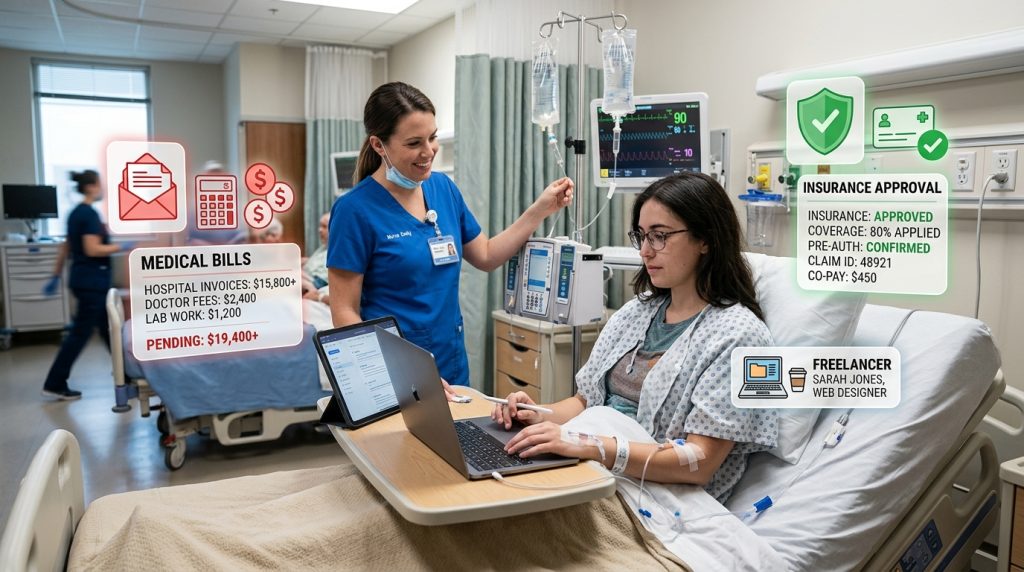

Real-Life Scenario

Imagine this:

You’re a freelancer earning ₹50,000/month.

Suddenly:

- You fall sick

- Can’t work for 2 months

- Hospital bill = ₹1 lakh

Without insurance:

- You lose ₹2 lakh income

- Plus ₹1 lakh expense

👉 Total loss = ₹3 lakh

With insurance?

- Hospital covered

- Income support continues

That’s the difference.

FAQs (People Also Ask)

1. Do freelancers really need insurance?

Yes. Freelancers don’t have employer benefits, so insurance is essential for financial security.

2. What is the most important insurance for freelancers?

Health insurance is the top priority, followed by income protection.

3. Is liability insurance necessary for freelancers?

Yes, especially if you work with clients. It protects against legal claims.

4. How much does freelancer insurance cost?

It varies, but basic health insurance can start from ₹8,000–₹15,000/year.

5. Can freelancers claim tax benefits on insurance?

Yes. Premiums paid for health and life insurance are eligible for tax deductions under Indian laws.