Buying life insurance feels like a smart move. And it is.

But here’s the catch—one wrong decision can quietly cost you lakhs over time.

Many people think they’re protected, but in reality, they’ve made small mistakes that turn into big financial losses later.

Let’s fix that today.

Why Life Insurance Mistakes Are So Expensive

Life insurance is a long-term commitment. You may pay premiums for 20–30 years.

So even a small mistake can:

- Increase your premium

- Reduce your coverage

- Or worse, leave your family unprotected

That’s why getting it right matters.

Mistake #1: Buying Too Little Coverage

This is the most common mistake.

People often choose a low coverage amount to save premium. But when something happens, that amount is simply not enough.

What You Should Do Instead:

- Aim for 10–15 times your annual income

- Factor in loans, kids’ education, and daily expenses

Example: If you earn ₹10 lakh/year, your cover should be at least ₹1–1.5 crore.

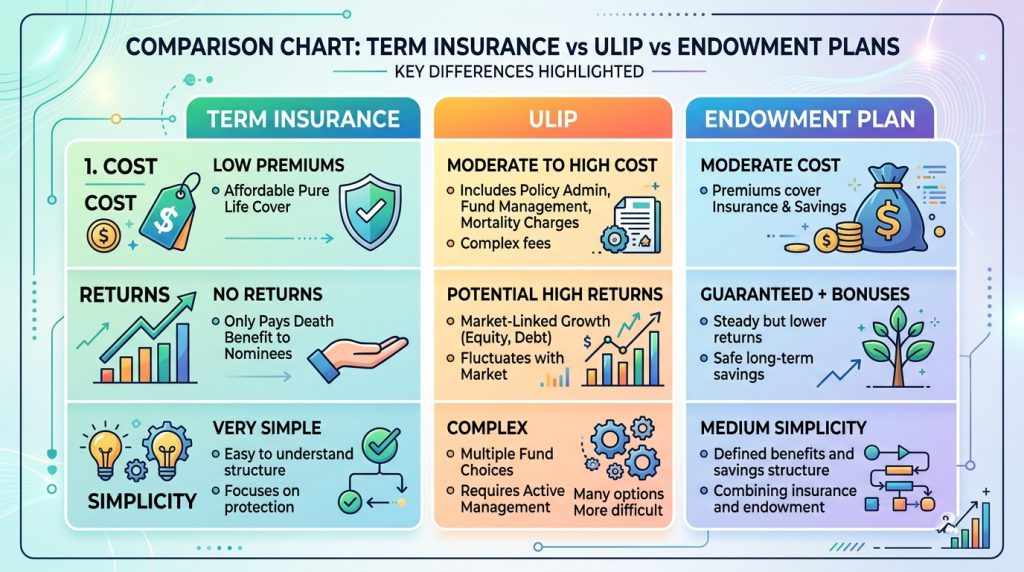

Mistake #2: Mixing Insurance with Investment

Plans like ULIPs or endowment policies sound attractive. They promise returns + insurance.

But in reality:

- Returns are often lower

- Premiums are higher

- Transparency is limited

Better Option:

Go for:

- Term Insurance (pure protection)

- Invest separately in mutual funds or SIPs

Mistake #3: Ignoring Policy Terms and Conditions

Most people don’t read the fine print. Big mistake.

Hidden clauses can include:

- Waiting periods

- Exclusions

- Claim conditions

What to Check:

- Suicide clause

- Pre-existing illness rules

- Claim process

Take 10 minutes now to avoid big regret later.

Mistake #4: Delaying Purchase

“I’ll buy next year.”

That one line can cost you thousands.

Why Delay Hurts:

- Premium increases with age

- Health risks may rise

- You may become ineligible

Smart Move:

Buy early, even if coverage is basic. You can upgrade later.

Mistake #5: Not Disclosing Correct Information

Some people hide details like:

- Smoking habits

- Medical history

It may reduce premium slightly. But it’s risky.

What Can Go Wrong:

- Claim rejection

- Policy cancellation

Always be 100% honest. It protects your family.

Mistake #6: Choosing the Wrong Policy Term

If your policy ends too early, your family is at risk.

Common Error:

Taking a 15–20 year policy when responsibilities last longer.

Ideal Approach:

- Cover should last till retirement (60–65 years)

- Match it with your earning years

Mistake #7: Not Reviewing Your Policy

Life changes. Your insurance should too.

But many people buy once and forget.

When to Review:

- Marriage

- Birth of a child

- Salary increase

- New loans

Simple Fix:

Review your policy every 2–3 years.

Quick Checklist to Avoid These Mistakes

| Mistake | Smart Fix |

|---|---|

| Low coverage | 10–15x annual income |

| Investment plans | Choose term insurance |

| Ignoring terms | Read policy details |

| Delaying | Buy early |

| Wrong info | Be honest |

| Short term | Cover till retirement |

| No review | Check every 2–3 years |

Pro Tips to Get the Best Life Insurance Plan

- Compare plans online before buying

- Check claim settlement ratio

- Choose a trusted insurer

- Avoid agents pushing high-commission plans

- Buy directly from official websites

FAQs (People Also Ask)

1. What is the biggest mistake in life insurance?

The biggest mistake is buying too little coverage, which fails to support your family financially.

2. Is term insurance better than other plans?

Yes. It offers high coverage at low cost and is the best for pure protection.

3. When is the best time to buy life insurance?

As early as possible. Younger age means lower premiums.

4. Can a claim be rejected?

Yes, if you hide information or break policy terms.

5. How often should I review my policy?

Every 2–3 years or after major life changes.

One Simple Truth

Life insurance is not just a policy. It’s a promise to your family.

Don’t let small mistakes break that promise.