Car insurance is one of those things you must have. But paying a high premium every year? That hurts.

Here’s the good news—you don’t have to choose between saving money and staying protected.

With the right moves, you can lower your car insurance premium without losing coverage. Let’s break it down in a simple, practical way.

Why Your Car Insurance Premium Feels So High

Before cutting costs, you need to know what’s driving the price.

Your premium depends on:

- Your car’s value

- Your driving history

- Location (city vs small town)

- Type of coverage

- Add-ons

Once you understand this, saving money becomes easier.

1. Increase Your Voluntary Deductible

A deductible is the amount you pay from your pocket during a claim.

How It Helps:

- Higher deductible = Lower premium

- You save money yearly

But Be Smart:

Choose a deductible you can afford in emergencies.

Example: Raising deductible from ₹2,000 to ₹5,000 can reduce premium significantly.

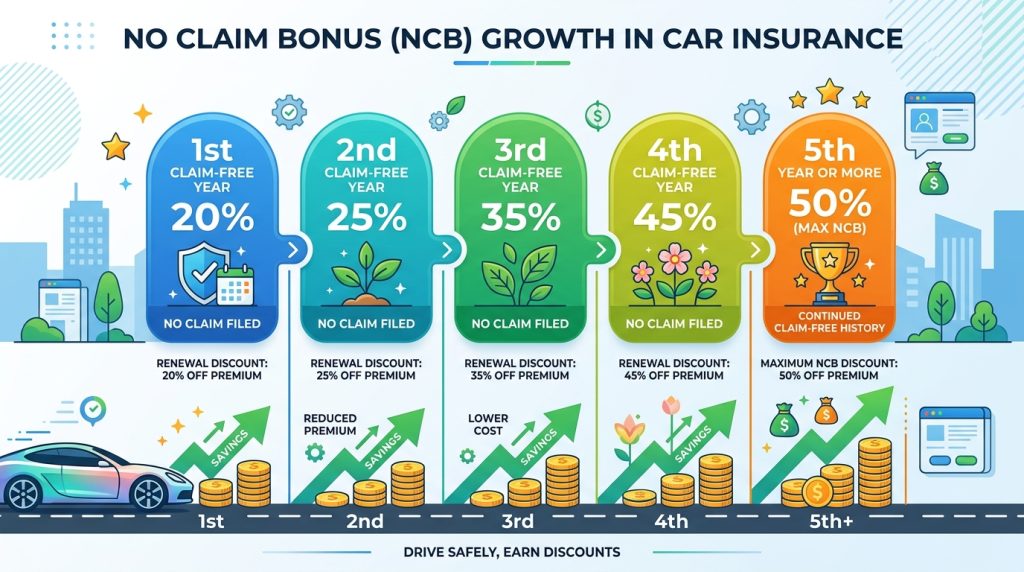

2. Avoid Small Claims (Protect Your NCB)

NCB stands for No Claim Bonus.

If you don’t make claims, your premium drops every year.

NCB Benefits:

- Starts at 20% discount

- Can go up to 50%

Smart Tip:

Avoid claiming for minor damages. Pay small repairs yourself.

3. Compare Policies Before Renewal

Many people renew without checking other options. That’s like leaving money on the table.

What to Do:

- Compare plans online

- Check features and price

- Look for discounts

Even switching insurers can save thousands.

4. Install Safety Devices in Your Car

Insurance companies love safer cars.

Devices That Help:

- Anti-theft alarm

- GPS tracker

- Steering lock

These reduce risk, so insurers reward you with lower premiums.

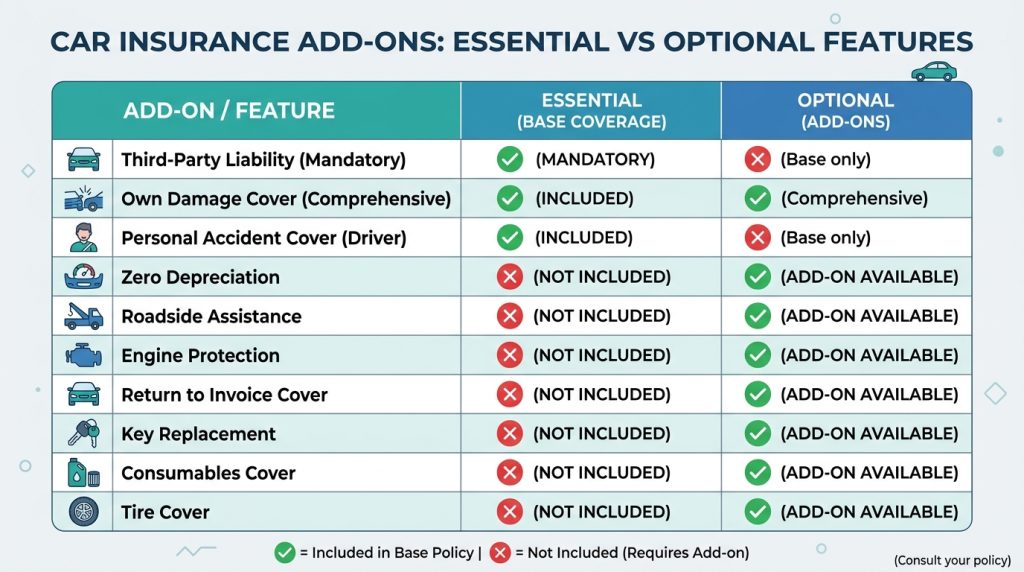

5. Choose Add-Ons Carefully

Add-ons are useful, but too many can increase your premium.

Common Add-Ons:

- Zero depreciation cover

- Engine protection

- Roadside assistance

Smart Move:

Only keep what you truly need.

Example: If your car is old, skip zero depreciation cover.

6. Maintain a Good Driving Record

Your driving behavior matters a lot.

If You:

- Avoid accidents

- Follow traffic rules

Then you’re seen as a low-risk driver.

Result? Lower premium over time.

7. Bundle Insurance Policies

If you buy multiple policies from the same insurer, you may get a discount.

Example:

- Car + bike insurance

- Car + health insurance

This can reduce your overall cost.

8. Don’t Over-Insure Your Car

Your car’s value decreases every year. This is called IDV (Insured Declared Value).

Common Mistake:

Keeping IDV too high.

Smart Move:

- Choose a realistic IDV

- Not too high, not too low

This directly affects your premium.

9. Renew Your Policy on Time

Missing renewal can cost you:

- Loss of NCB

- Higher premium

- Inspection charges

Tip:

Set a reminder 1–2 weeks before expiry.

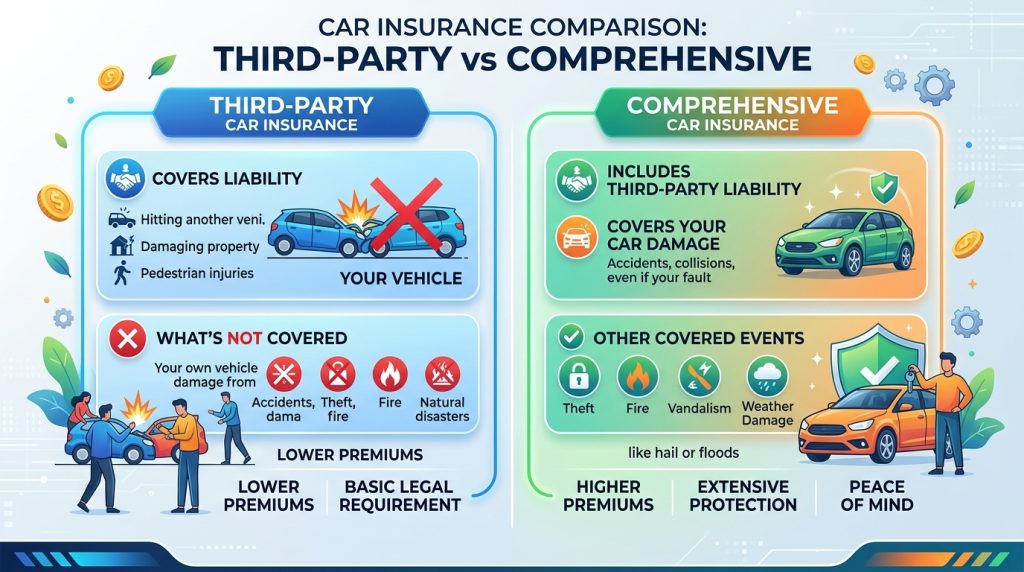

10. Choose the Right Coverage Type

There are two main types:

| Type | Coverage | Cost |

|---|---|---|

| Third-Party | Basic legal cover | Low |

| Comprehensive | Full protection | Higher |

Best Choice:

Go for comprehensive, but optimize it with smart add-ons.

Quick Checklist to Reduce Premium

- Increase deductible

- Avoid small claims

- Compare before renewal

- Install safety devices

- Remove unnecessary add-ons

- Drive safely

- Adjust IDV wisely

Real Example: How You Can Save

Let’s say your current premium is ₹15,000/year.

By doing this:

- Increase deductible → Save ₹2,000

- Maintain NCB → Save ₹3,000

- Remove add-ons → Save ₹2,000

👉 Total savings = ₹5,000–₹7,000 per year

Pro Tips Most People Don’t Know

- Buy insurance online (cheaper than agents)

- Check for festive discounts

- Use long-term policies for better rates

- Always read policy terms before buying

FAQs (People Also Ask)

1. How can I reduce my car insurance premium?

You can lower it by increasing deductible, maintaining NCB, comparing policies, and removing unnecessary add-ons.

2. Does increasing deductible reduce premium?

Yes. A higher deductible means lower premium, but you pay more during claims.

3. What is the fastest way to save on car insurance?

Avoid small claims and maintain your No Claim Bonus.

4. Is it safe to remove add-ons?

Yes, if they are not useful for your car or driving needs.

5. Can I change my insurance company during renewal?

Yes. You can switch insurers easily and still keep your NCB.

One Simple Rule

Don’t just pay your premium. Control it.

A few smart decisions today can save you thousands every year—without risking your protection.